Opinion

Central Bank Implementation of Digital Cash and Economic Impact

—

As seen in: Stern in the News

By Haran Segram, Carmelle Cadet, Evgeni Mitkov, and Diane Maurice

Billions of individuals and businesses are grossly underserved by the banking sector. The COVID-19 pandemic, and an arms race to deliver central bank issued digital currency (CDBC) are making most central banks consider issuing digital versions of their fiat currencies. We propose a Digital Cash Infrastructure for all, and have highlighted the essential role of cash in every economy. Cash as a payment instrument and store of value is trusted, accessible, riskless and broadly used in peer to peer payments (PND White Paper, 2020).

Central banks have always been tasked with financial inclusion; now, they can also deliver it. The technology now exists to allow a central bank to issue and deliver digital cash to an individual’s wallet and for that digital cash to circulate in the economy just like paper cash. This financial infrastructure closes the unbanked gap with core digital currency services (wallets, person to person payments, benefit payments, etc.) For most Central Banks, financial inclusion is as important as promoting price stability, financial stability and in some cases full employment.

Central banks issue paper cash today, but as the world becomes more digital, paper cash is becoming more limiting, inefficient, and continues to be costly. Yet, cash is used in 30% of payments globally, only 18% of the global population has credit cards and over 2 billion are unbanked or underbanked. An estimated 10% of the world’s GDP (~$10 trillion USD) is in physical cash.

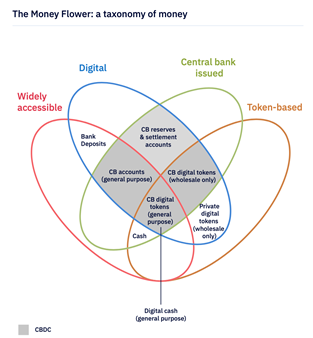

The Bank of International Settlements defines a Central Bank Digital Currency as a “digital form of central bank money that is different from balances in traditional reserve or settlement accounts (i.e. balances in accounts held by commercial banks at the central bank).”

We propose the Federal Reserve as an example, could adopt blockchain technology and distributed ledgers to tokenize a segment of its money supply to serve as a legal tender that is accessible to everyone. This “Cash-Like” model of CBDC with privacy and instant final settlement is key to closing the inclusion gap. It retains paper cash features, and enables bank-like and mobile money services to reach the unbanked or underbanked segments of the economy, but much more efficiently. That efficiency can make payments free for any cash user, while accessing value add services (loans, payroll, investing, etc.) in the private sector.

For a central bank, implementation of a digital cash solution can begin as a standalone add-on to the central bank toolbox, designed with a robust regulatory framework. A value proposition for central banks is to align traditional mandates of price and financial stability with a modern technology to create, distribute and manage cash. Effectively adopting a software that issues a token on a digital ledger, instead of printing and stocking them in warehouses or vaults. Faster and more efficient digital payments provide better data and enhance the central bank's understanding of the economy, and its ability to control money laundering, without violating citizens’ privacy.

Technology

We recommend that central banks should seek out action-oriented technology and frameworks to transform financial market infrastructure. The platform should offer Digital Cash that transcends traditional payment infrastructure, FX markets and blockchain-based payments, and streamlines the Digital Cash Token Lifecycle Management, Private Transaction Network and Digital Cash Access Tools: APIs, Smart Contracts, Apps, etc. (PND White Paper, 2020).

The digital cash blockchain and APIs create a mechanism to issue and manage a country’s currency to accelerate goals for financial inclusion. The smart contract solutions endorse standard Central Bank commitment to developing a ‘repeatable and verifiable’ process in governance and compliance. But, testing and implementation strategies can be challenging.

To that end, central banks should deploy a digital innovation sandbox that balances both the central bank’s conservative and cautious posture with increasing demands for innovation. The sandbox solution provides a safety value for any central bank, including the Federal Reserve, to test various components with consumer-facing solutions and innovators.

In executing new technology, Central Banks must first and foremost consider new risk metrics; the sandbox solution provides a safe entry into new financial market infrastructures that is developing exponentially. Central bank policy and implementation of transitional improvements typically lag the market, but we consider actionable solutions that promote controlled innovations to challenge these trends. Maintaining confidence and trust underscores this approach.

Economic Policy & Impact

Income Inequality

Before this crisis, Brynjolfsson and McAfee described what they called the “Great Decoupling” where wages and productivity were highly correlated from 1947 to 1973, but post-1973 productivity doubled but wages were stagnant. This pandemic has impacted the low-income families disparately, somewhat different from previous economic downturns like the Great Decoupling. For example, 40% of the households earning $40,000 (USD) or less have lost their jobs or furloughed (Powell, 2020). COVID-19 has exposed various gaps in the U.S. financial market and in anticipation of the institution of a ‘minimum income’ policy to mitigate the ever-growing income divide, we urge Congressional Leaders to call for a modern and inclusive financial market infrastructure that is accessible to everyone.

Existence of CBDC as a Digital Cash instrument and associated digital wallet can:

Health

Income inequality and associated social divide is causing an irreparable health crisis. Importantly, empirical evidence suggests that the top stressors included money, work, and the economy, with 61% of Americans reporting money as a stressor. Moreover, Americans with lower incomes reported a disproportionately higher amount of stress and higher inability to manage stress (Layte, 2011, Segram and Sequeira, 2020). The extant empirical research supports the notion that lack of financial security leads to both physical and mental ailments. Narrowing the income inequality gap will eventually lead to savings in healthcare costs in the long-term, although it is noted that the immediate solution to healthcare challenges is a public option.

Competitiveness

The modern cold war between the U.S. and China and race to superiority revolves around maintaining the reserve currency status and technology. At present, U.S. dollars account for more than 60% of all foreign currency reserves in the world.

If the US Dollar loses that reserve currency status, during the next pandemic, the U.S treasury might not be able to access the global debt markets with at most ease it did all though COVID-19. Moreover, the ability to fund our ever increasing national deficit becomes restricted. A Bank of England study has found that CBDC being 30% of the GDP could possibly lead to 3% increase GDP due to savings in transaction costs, lowering real interest rates and distortionary taxes. The PBOC moving to digital yuan and possibly becoming the world’s reserve currency is an existential threat to the U.S. progress.

Our goal to transform central banking is driven by our passion for financial inclusion. The worlds’ financial system relies on a central banking model for safety and stability. We believe a digital cash infrastructure built with central bank digital currency will close the financial inclusion gap. Our combined expertise and knowledge of blockchain virtually eradicates the lack of access to basic, safe and low-cost finance in any market.

Access to blockchain-based digital cash, regardless of whether someone has a bank account or not, is the structural democratization of money.

____

Haran Segram is Clinical Assistant Professor of Finance. Carmelle Cadet is the Founder & CEO of EMTECH. Evgeni Mitkov is the CTO of EMTECH. Diane Maurice is the Chief Policy Advisor of EMTECH

Central banks have always been tasked with financial inclusion; now, they can also deliver it. The technology now exists to allow a central bank to issue and deliver digital cash to an individual’s wallet and for that digital cash to circulate in the economy just like paper cash. This financial infrastructure closes the unbanked gap with core digital currency services (wallets, person to person payments, benefit payments, etc.) For most Central Banks, financial inclusion is as important as promoting price stability, financial stability and in some cases full employment.

Central banks issue paper cash today, but as the world becomes more digital, paper cash is becoming more limiting, inefficient, and continues to be costly. Yet, cash is used in 30% of payments globally, only 18% of the global population has credit cards and over 2 billion are unbanked or underbanked. An estimated 10% of the world’s GDP (~$10 trillion USD) is in physical cash.

The Bank of International Settlements defines a Central Bank Digital Currency as a “digital form of central bank money that is different from balances in traditional reserve or settlement accounts (i.e. balances in accounts held by commercial banks at the central bank).”

We propose the Federal Reserve as an example, could adopt blockchain technology and distributed ledgers to tokenize a segment of its money supply to serve as a legal tender that is accessible to everyone. This “Cash-Like” model of CBDC with privacy and instant final settlement is key to closing the inclusion gap. It retains paper cash features, and enables bank-like and mobile money services to reach the unbanked or underbanked segments of the economy, but much more efficiently. That efficiency can make payments free for any cash user, while accessing value add services (loans, payroll, investing, etc.) in the private sector.

For a central bank, implementation of a digital cash solution can begin as a standalone add-on to the central bank toolbox, designed with a robust regulatory framework. A value proposition for central banks is to align traditional mandates of price and financial stability with a modern technology to create, distribute and manage cash. Effectively adopting a software that issues a token on a digital ledger, instead of printing and stocking them in warehouses or vaults. Faster and more efficient digital payments provide better data and enhance the central bank's understanding of the economy, and its ability to control money laundering, without violating citizens’ privacy.

Technology

We recommend that central banks should seek out action-oriented technology and frameworks to transform financial market infrastructure. The platform should offer Digital Cash that transcends traditional payment infrastructure, FX markets and blockchain-based payments, and streamlines the Digital Cash Token Lifecycle Management, Private Transaction Network and Digital Cash Access Tools: APIs, Smart Contracts, Apps, etc. (PND White Paper, 2020).

The digital cash blockchain and APIs create a mechanism to issue and manage a country’s currency to accelerate goals for financial inclusion. The smart contract solutions endorse standard Central Bank commitment to developing a ‘repeatable and verifiable’ process in governance and compliance. But, testing and implementation strategies can be challenging.

To that end, central banks should deploy a digital innovation sandbox that balances both the central bank’s conservative and cautious posture with increasing demands for innovation. The sandbox solution provides a safety value for any central bank, including the Federal Reserve, to test various components with consumer-facing solutions and innovators.

In executing new technology, Central Banks must first and foremost consider new risk metrics; the sandbox solution provides a safe entry into new financial market infrastructures that is developing exponentially. Central bank policy and implementation of transitional improvements typically lag the market, but we consider actionable solutions that promote controlled innovations to challenge these trends. Maintaining confidence and trust underscores this approach.

Economic Policy & Impact

Income Inequality

Before this crisis, Brynjolfsson and McAfee described what they called the “Great Decoupling” where wages and productivity were highly correlated from 1947 to 1973, but post-1973 productivity doubled but wages were stagnant. This pandemic has impacted the low-income families disparately, somewhat different from previous economic downturns like the Great Decoupling. For example, 40% of the households earning $40,000 (USD) or less have lost their jobs or furloughed (Powell, 2020). COVID-19 has exposed various gaps in the U.S. financial market and in anticipation of the institution of a ‘minimum income’ policy to mitigate the ever-growing income divide, we urge Congressional Leaders to call for a modern and inclusive financial market infrastructure that is accessible to everyone.

Existence of CBDC as a Digital Cash instrument and associated digital wallet can:

- Digitize Cash-based or check-based payments (payroll, refunds, benefits, etc.)

- Streamline the implementation of UBI

- Facilitate peer to peer transfers of digital cash

- Drastically lower the intermediation costs for the Federal Reserve, individuals and small businesses who use cash

Health

Income inequality and associated social divide is causing an irreparable health crisis. Importantly, empirical evidence suggests that the top stressors included money, work, and the economy, with 61% of Americans reporting money as a stressor. Moreover, Americans with lower incomes reported a disproportionately higher amount of stress and higher inability to manage stress (Layte, 2011, Segram and Sequeira, 2020). The extant empirical research supports the notion that lack of financial security leads to both physical and mental ailments. Narrowing the income inequality gap will eventually lead to savings in healthcare costs in the long-term, although it is noted that the immediate solution to healthcare challenges is a public option.

Competitiveness

The modern cold war between the U.S. and China and race to superiority revolves around maintaining the reserve currency status and technology. At present, U.S. dollars account for more than 60% of all foreign currency reserves in the world.

If the US Dollar loses that reserve currency status, during the next pandemic, the U.S treasury might not be able to access the global debt markets with at most ease it did all though COVID-19. Moreover, the ability to fund our ever increasing national deficit becomes restricted. A Bank of England study has found that CBDC being 30% of the GDP could possibly lead to 3% increase GDP due to savings in transaction costs, lowering real interest rates and distortionary taxes. The PBOC moving to digital yuan and possibly becoming the world’s reserve currency is an existential threat to the U.S. progress.

Our goal to transform central banking is driven by our passion for financial inclusion. The worlds’ financial system relies on a central banking model for safety and stability. We believe a digital cash infrastructure built with central bank digital currency will close the financial inclusion gap. Our combined expertise and knowledge of blockchain virtually eradicates the lack of access to basic, safe and low-cost finance in any market.

Access to blockchain-based digital cash, regardless of whether someone has a bank account or not, is the structural democratization of money.

____

Haran Segram is Clinical Assistant Professor of Finance. Carmelle Cadet is the Founder & CEO of EMTECH. Evgeni Mitkov is the CTO of EMTECH. Diane Maurice is the Chief Policy Advisor of EMTECH